Security Provision and Economic Entrenchment in the Gulf: Toward a Bifurcated Hegemonic Order

Why the 2026 Iran War Is Splitting the Gulf Between American Security and Chinese Power

Abstract

Escalatory cycles between Israel and Iran, the regional spillover from the October 2023 Gaza war, persistent attacks on Gulf energy infrastructure, and renewed US force deployments have re-intensified debate over Middle Eastern order. While much scholarship focuses on deterrence dynamics and balance-of-power shifts, this article argues that a deeper structural transformation is underway. The Gulf energy system is increasingly organised around a bifurcated external hegemony: the United States continues to underwrite the region’s security layer, while China consolidates its position within its economic and infrastructural layer.

Drawing on hegemonic stability theory, complex interdependence, and infrastructure resilience analysis, the article contends that this functional division of labour—security provision by Washington, reconstruction and capital deployment by Beijing—may stabilise regional energy flows in the short term while embedding long-term strategic asymmetry. Using Iraq as the principal case study and analysing one-, five- and ten-year horizons, the article explores how a model of “functional dual hegemony” may become the organising logic of Gulf order. It concludes that although this arrangement may appear efficient and attractive to regional elites, it is structurally fragile and strategically unstable.

1. Introduction

The Gulf has entered a renewed period of strategic volatility. The October 2023 Gaza war triggered regional escalation, including attacks by Iranian-aligned armed groups against US forces in Iraq and Syria, maritime insecurity in the Red Sea, and heightened threats to energy infrastructure (International Crisis Group, 2024; US Department of Defense, 2024). These developments revived memories of earlier shocks such as the 2019 Abqaiq–Khurais attacks on Saudi oil facilities, which temporarily removed approximately 5 per cent of global oil supply (Energy Information Administration, 2019).

Simultaneously, the United States has maintained and, at times, reinforced its force posture in the region, integrating air and missile defence capabilities with Gulf partners and sustaining naval patrols in key maritime corridors (US Department of Defense, 2024). Despite periodic narratives of American retrenchment, Washington remains the only actor capable of providing large-scale kinetic deterrence and maritime security in the Gulf.

At the same time, China’s economic footprint across the Middle East has deepened significantly. Chinese national oil companies (NOCs) hold major stakes in Iraqi oilfields; Chinese state-linked enterprises participate in infrastructure, power generation, ports and transport projects; and commodity-linked financing mechanisms have expanded Beijing’s structural influence (Downs, 2023; Aziz and Salih, 2026).

These parallel developments raise a structural question: is the Gulf evolving toward a bifurcated form of hegemony in which security and economic authority are supplied by different external powers?

Hegemonic stability theory traditionally posits that international systems function most effectively when a single dominant power supplies public goods such as security and financial stability (Kindleberger, 1973; Gilpin, 1981). However, the contemporary Gulf energy system exhibits layered interdependence. Its security layer, deterrence, missile defence, sea-lane protection, remains overwhelmingly American. Its economic layer, capital flows, infrastructure construction, long-term commodity demand, is increasingly shaped by China.

This article advances three claims:

The Gulf energy system is structurally layered, and these layers are now underwritten by different powers.

Iraq represents the clearest case of this bifurcated arrangement in practice.

Over a ten-year horizon, this division of labour may stabilise into managed dual hegemony, drift toward Sino-centric economic leverage, or fragment under sustained insecurity and governance failure.

2. The Gulf Energy System as a Layered Resilience Architecture

Energy security is often discussed in terms of supply volume and price stability. However, the Gulf energy system is more accurately understood as an integrated resilience architecture. It consists of:

Upstream production

Export terminals and loading infrastructure

Pipelines and compression stations

Power generation and water systems

Maritime transit corridors

Financial clearing and insurance mechanisms

These components form an interdependent network. Disruption in one node, whether kinetic attack, cyber interference or political instability, can cascade through the system.

The 2019 Abqaiq–Khurais attacks demonstrated the vulnerability of high-consequence nodes (EIA, 2019). Similarly, Houthi attacks on Red Sea shipping in 2023–24 illustrated how maritime insecurity can rapidly reprice global trade routes (International Crisis Group, 2024).

Resilience therefore depends on two distinct capabilities:

Deterrence and force protection

Rapid restoration and reconstruction

The United States specialises in the former; China increasingly specialises in the latter.

3. Sanctions Arbitrage and Structural Exposure

China’s energy procurement strategy over the past decade has included significant volumes from politically isolated or sanctioned producers, including Iran and Venezuela (Downs, 2023). Discounted barrels provide economic advantage and geopolitical leverage. However, this strategy carries exposure if geopolitical shocks disrupt supply channels.

When escalation increases maritime risk or prompts enforcement tightening, discounted supply becomes vulnerable. The broader lesson is structural: arbitrage strategies are resilient against incremental sanctions pressure but fragile under kinetic disruption.

This creates an incentive for Beijing to deepen its position in suppliers where long-term stakes are institutionalised and internationally normalised. Iraq, as OPEC’s second-largest producer, offers precisely such an opportunity.

4. US Security Reassertion After 2026

The strikes and subsequent escalation have re-centred US military power in the Gulf. Reporting indicates:

Force surges across naval and air domains

Reinforced missile defence integration

Refusal to exclude ground deployment options (Washington Post, 2026)

Brookings (2026) frames this as a reaffirmation of American willingness to use hard power to stabilise energy-critical regions.

In hegemonic terms, this is classic security public goods provision. Regional states, despite prior hedging, remain dependent on American kinetic capacity for deterrence.

However, security dominance does not equate to economic dominance. Fiscal constraints, domestic political fatigue, and ESG pressures limit large-scale Western reconstruction financing (MERICS, 2025).

This creates a structural opening.

5. China’s Economic Entrenchment and the Iraq Case

China’s energy strategy prior to the war relied in part on discounted barrels from sanctioned producers (Garcia-Herrero, 2026; USCC, 2026). The disruption of Iranian exports exposes vulnerability in that model.

Beijing’s rational adaptation is to deepen structural embedding in producers with greater international legitimacy, most notably Iraq.

According to Atlantic Council analysis (2025; 2026):

Chinese firms hold stakes in major Iraqi fields

Infrastructure projects link oil exports to Chinese finance

“Oil-for-infrastructure” models create long-term leverage

This entrenchment operates across both upstream and enabling infrastructure.

Unlike the United States, China does not deploy combat brigades. It deploys:

Policy bank financing

Construction conglomerates

Long-term purchase contracts

In resilience terms, the US absorbs escalation risk; China absorbs capital risk.

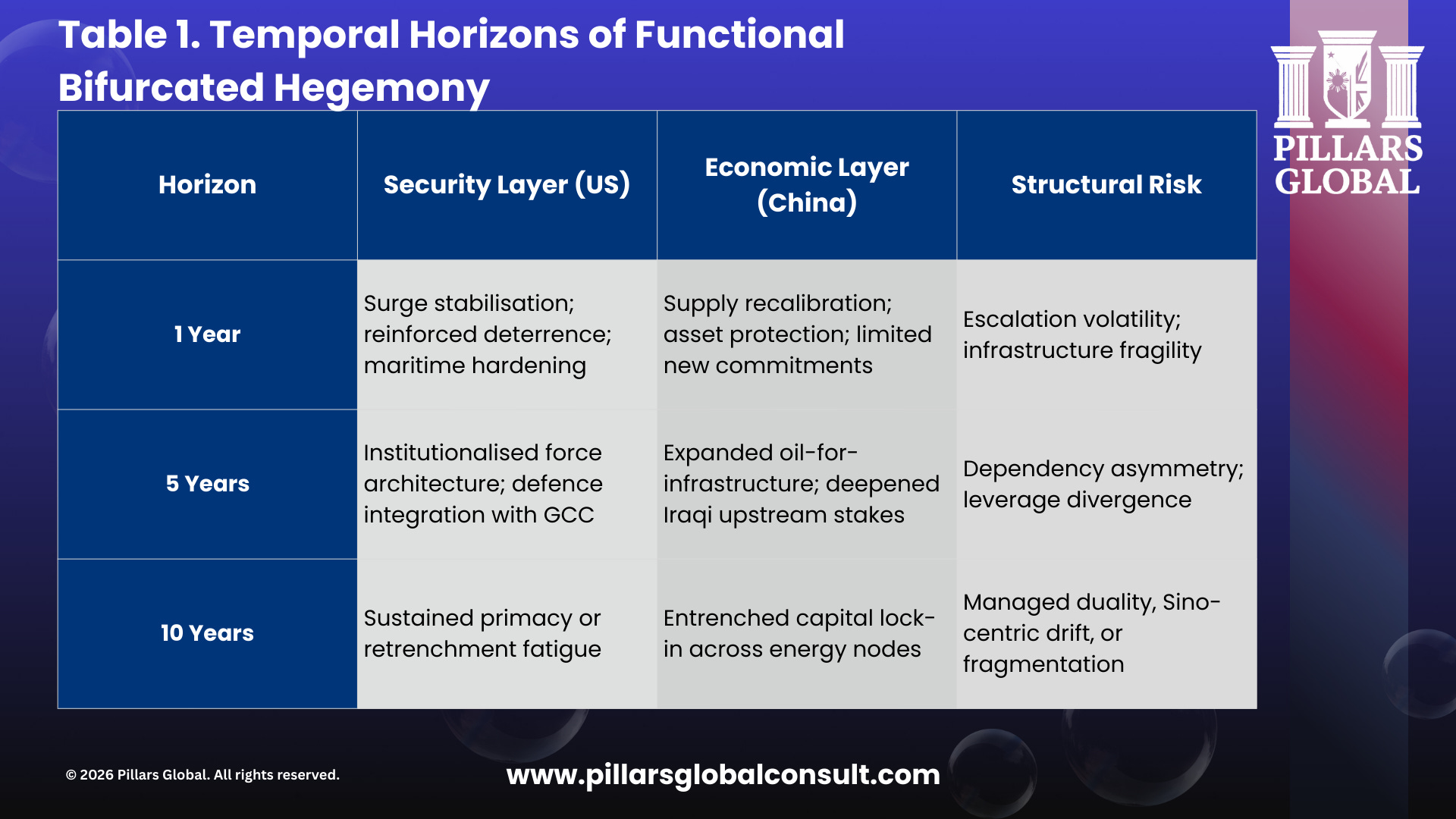

6. Temporal Evolution of Bifurcated Hegemony

To evaluate whether bifurcated hegemony represents a transitional anomaly or an enduring structure, temporal differentiation is essential. The strategic meaning of 2026 differs across one-year, five-year and ten-year horizons.

6.1 One-Year Horizon: Shock Absorption

In the immediate phase, American primacy is uncontested. Force projection, missile interception, and maritime stabilisation dominate the agenda. Oil markets remain volatile but operational flows resume under security cover (Reuters, 2026a).

China’s posture in this period is reactive and protective. Beijing avoids direct confrontation, focuses on safeguarding existing investments, and recalibrates supply chains. The emphasis is risk containment rather than expansion.

The system stabilises, but resilience remains shallow. Infrastructure remains exposed to renewed escalation, and structural repair is incomplete.

Bifurcation exists but remains asymmetric: Washington bears escalation risk; Beijing absorbs market volatility.

6.2 Five-Year Horizon: Institutional Consolidation

Over five years, crisis response evolves into structural architecture.

The United States formalises an expanded defence posture. Integrated air defence networks deepen across GCC states, and maritime patrols become institutionalised. Security public goods are routinised.

Simultaneously, Chinese economic engagement deepens. Oil-for-infrastructure frameworks expand in Iraq, tying export flows to long-term capital deployment (Atlantic Council, 2026). Chinese firms embed across additional infrastructure nodes.

The result is structural asymmetry: Gulf states depend on Washington for survival in high-intensity scenarios while depending on Beijing for growth and reconstruction.

This phase represents the consolidation of functional bifurcation.

6.3 Ten-Year Horizon: Structural Outcomes

Beyond five years, three trajectories become plausible.

Managed Dual Hegemony

Security and economic layers remain separated but coordinated. Regional states successfully hedge, extracting benefits from both powers. Energy markets remain globally integrated.

Creeping Sino-Centric Drift

Over time, accumulated infrastructure ownership and commodity-linked finance give China leverage over routing decisions, pricing preferences and political alignments (MERICS, 2025). While US military primacy persists, economic gravity shifts.

Fragmentation

Alternatively, sustained insurgency, domestic political fatigue in the United States, or escalating great-power rivalry undermine both layers. If security commitments weaken while infrastructure remains exposed, volatility returns.

The ten-year horizon reveals bifurcation as a contingent equilibrium rather than a stable end state.

7. Risk Transfer and Strategic Asymmetry

The phrase “US breaks, China builds” requires analytical sharpening.

This is not burden sharing. It is risk differentiation.

The United States absorbs kinetic escalation risk, reputational exposure, and force-protection costs.

China absorbs capital exposure, long-duration debt risk, and infrastructure vulnerability.

Both powers externalise different forms of risk into the same geography.

However, long-term influence accrues disproportionately to the actor embedded in structural systems rather than episodic intervention. Infrastructure lock-in generates cumulative leverage.

Western anxiety therefore centres not on Chinese military deployment but on structural entrenchment.

8. Systemic Stability and Coordination Gaps

Classical hegemonic systems align security and economic authority within one actor (Gilpin, 1981). The Gulf’s emerging architecture separates these functions.

This separation creates coordination gaps:

Security decisions may not align with infrastructure priorities.

Reconstruction may proceed without parallel hardening.

Economic dependency may constrain strategic autonomy.

The system functions so long as both powers sustain commitment and competition remains bounded. Should either pillar weaken, systemic fragility intensifies.

9. Conclusion

The 2026 escalation accelerates an existing structural transformation.

The United States reasserts uncontested security primacy.

China deepens economic and infrastructural entrenchment.

The Gulf is not transitioning from one hegemon to another. It is dividing between them.

This bifurcated order may stabilise flows in the medium term, but it embeds asymmetry and interdependence that complicate long-term stability.

The next decade will determine whether functional bifurcation evolves into managed duality, Sino-centric economic gravity, or renewed fragmentation.

What is clear is that the organising logic of the post-war Gulf energy order is no longer singular hegemony it is layered power.

References

Atlantic Council (2025) Why China is here to stay in Iraq’s energy sector. 4 November. Available at: https://www.atlanticcouncil.org/blogs/menasource/why-china-is-here-to-stay-in-iraqs-energy-sector/

Atlantic Council (2026) In Iraq, China’s long game unfolds. 25 January. Available at: https://www.atlanticcouncil.org/in-depth-research-reports/report/in-iraq-chinas-long-game-unfolds/

BBC (2026) ‘Oil and gas prices jump as Middle East conflict escalates’. 1 March. Available at: https://www.bbc.com/news

Brookings Institution (2026) ‘After the strike: The danger of war in Iran’. 2 March. Available at:

Chatham House (2026) ‘The Iran war and regional order’. 1 March. Available at:

Downs, E.S. (2023) China’s energy footprint in the Middle East. Washington, DC: Brookings Institution. Available at:

Energy Information Administration (2019) Saudi Arabia’s Abqaiq and Khurais attacks temporarily disrupted global oil supply. Available at: https://www.eia.gov/todayinenergy/detail.php?id=41021

Garcia-Herrero, A. (2026) ‘Iran: A bigger headache for China than Venezuela’. Available at: https://asiamacro.substack.com

Gilpin, R. (1981) War and Change in World Politics. Cambridge: Cambridge University Press.

International Crisis Group (2024) The Red Sea attacks and regional escalation. Available at:

Keohane, R.O. and Nye, J.S. (1977) Power and Interdependence. Boston: Little, Brown.

Kindleberger, C.P. (1973) The World in Depression 1929–1939. Berkeley: University of California Press.

MERICS (2025) Interests first: China’s playbook for post-conflict reconstruction. Mercator Institute for China Studies. Available at:

Peacediplomacy (2025) ‘China’s expanding influence in the Middle East’. Available at: https://www.peacediplomacy.org

Reuters (2026a) ‘Iran war throws oil market into biggest crisis in decades’. 28 February. Available at:

https://www.reuters.com

Security in Context (2025) ‘China, the United States, and Middle East geopolitics’. Available at:

https://www.securityincontext.org

United States–China Economic and Security Review Commission (USCC) (2026) China–Venezuela fact sheet. Available at:

https://www.uscc.gov

US Department of Defense (2024) CENTCOM posture statement. Available at:

https://www.defense.gov

Washington Post (2026) ‘U.S. won’t rule out sending ground troops into Iran’. 2 March. Available at:

https://www.washingtonpost.com